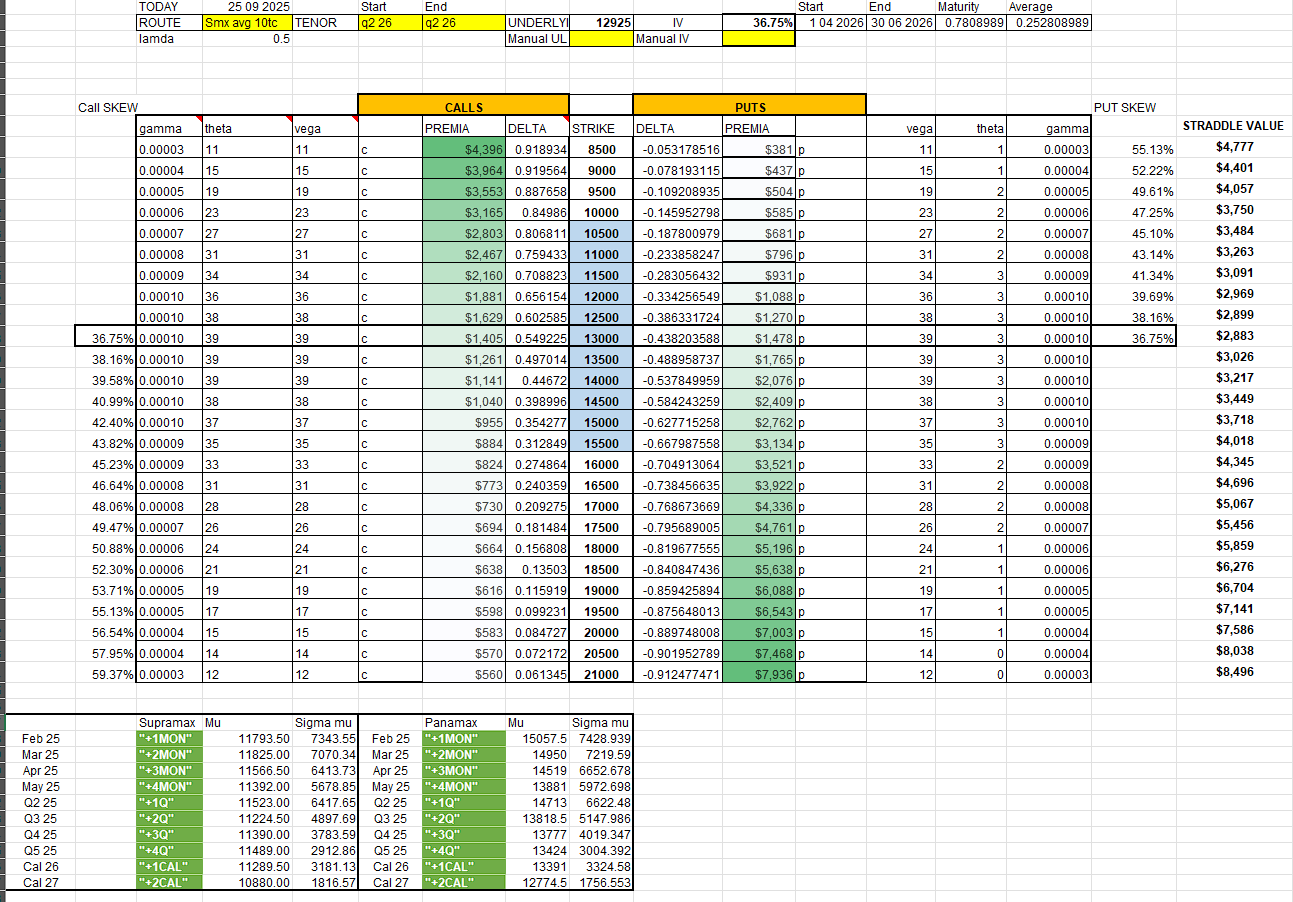

Asian options

Limitations of delta/gamma hedging

Asian options—whose value depends on the average price of an underlying asset—occupy a unique place in finance. They ride the fault line between classic derivatives theory and the messy realities of commodities, FX, and energy trading. Their averaging feature dampens volatility, reduces manipulation risk at expiry, but also demands sophisticated methods for valuation and hedging.

Section 1: The Basics—What Are Asian Options?

An Asian option pays out based on the average price of the underlying asset over some period, not its value at maturity. Formally:

Arithmetic average option: payoff is max(A−K,0)max(A−K,0), where

A = mean price across a time interval,

K = strike.

Geometric average option: average prices by their product’s root, less common but often easier to handle mathematically.

This averaging creates smoother risk and payout profiles, shielding end-users from price spikes at expiry. It explains their popularity in illiquid commodities and FX, where single-day manipulation is a threat.