Drift Is a Promise. Volatility Is the Delivery.

On short horizons, the risk-free rate is noise.

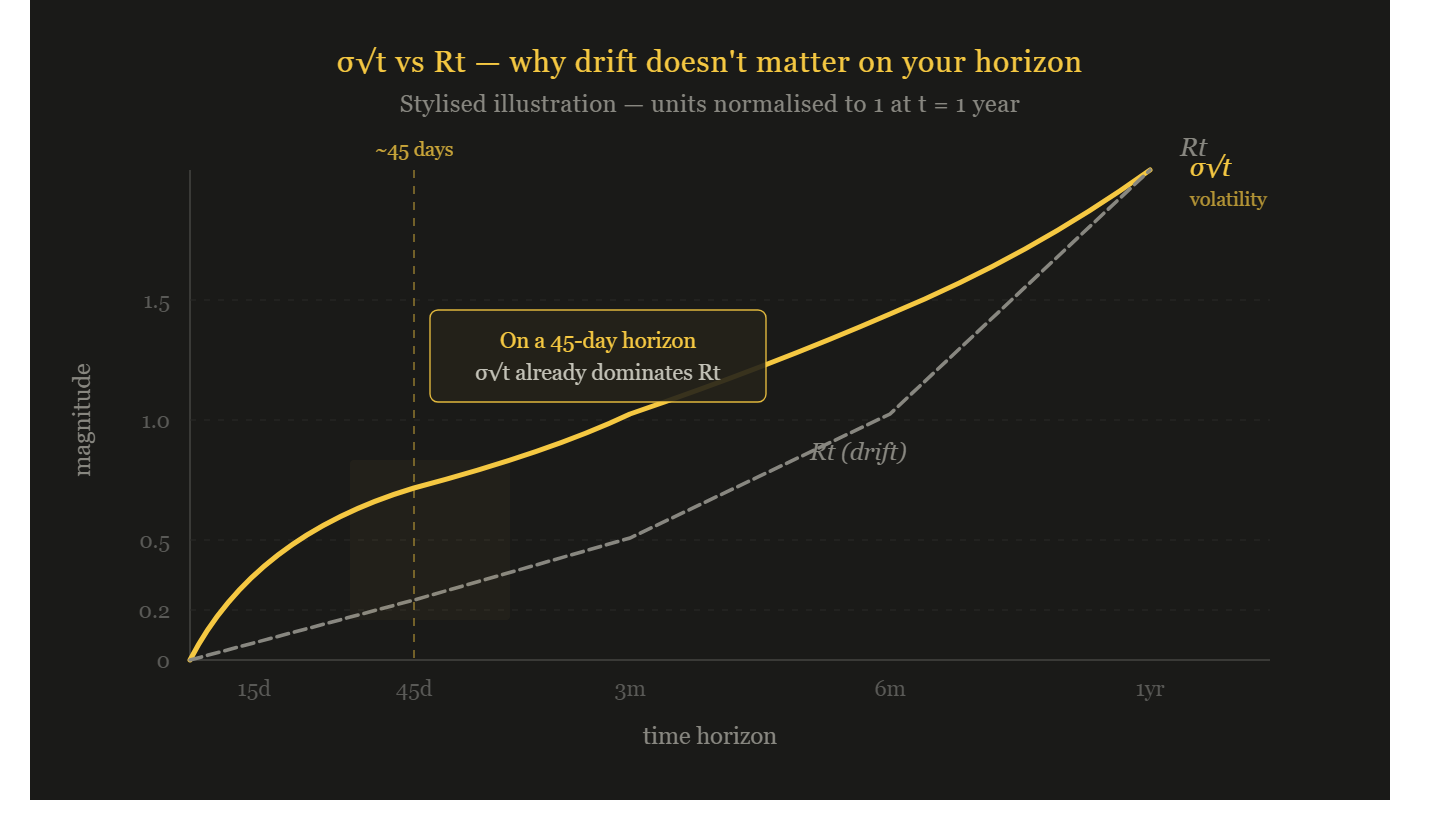

There is a confusion that sits at the centre of how most people think about markets, and it is not the usual confusion between correlation and causation, or between risk and uncertainty. It is more foundational than that. It is a confusion between two entirely different mathematical properties that happen to point in the same direction — and that coincidence has been expensive for a lot of people. The two properties are expected drift and probabilistic drift. They sound identical. They are not. Disentangling them is not an academic exercise. It changes how you position, what you hedge, and whether you survive the kind of environment we are currently inside.

Financial mathematics runs, almost entirely, on two assumptions. The first is the efficient market hypothesis — not in the naive form that markets are always correct, but in the technically relevant sense that prices are arbitrage-free. If they were not, you would not do financial mathematics at all. You would simply find the arbitrage and extract it until it disappeared. The entire apparatus of options pricing, forward curves, and risk-neutral valuation depends on this single condition: that you cannot manufacture riskless profit from price discrepancies. Accept that, and prices today become the discounted expected value of prices tomorrow. That is what the efficient market hypothesis actually delivers, mathematically speaking. The second assumption is the Markov property, which applies to Brownian motion, geometric Brownian motion, Black-Scholes, and virtually every stochastic differential equation model used in practice. What it says, precisely, is that the process is memoryless. The current price already encodes the full history of how it got there. The trajectory is irrelevant. What matters is where you are now, not where you have been. This is convenient, because it means you can treat every moment as a fresh start. It is also unsettling, because it means that reversions to historical levels carry no mathematical guarantee. Layer on the law of large numbers and you reach the comfortable conclusion: over long horizons, markets drift upward by approximately the risk-free rate. Positive drift. The theoretical underpinning for passive investing, for pension fund actuarial assumptions, for every financial product built around the idea that time in the market beats timing the market. All of that is true. And none of it helps you over the next 45 days.