Geometry of Decline

Aftermath of 2008

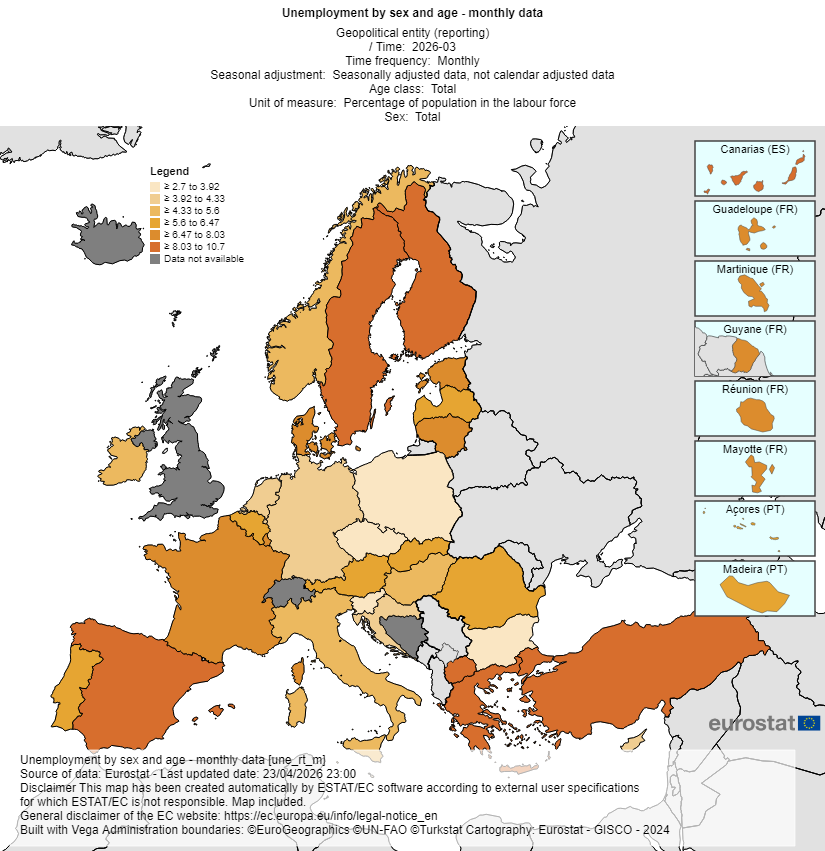

There is a particular kind of historical violence that does not announce itself with armies or fire, and Europe is currently inside one. The continent is sleepwalking through what future economic historians will almost certainly mark as the opening of a long arc of decline, and the strange thing is that the moment of inflection has already happened — it happened in 2008 — but the patient still believes the cancer is in remission because the cortisone is doing its theatrical work. Equity prices in Frankfurt are fine. Greek government bonds trade at yields that would have seemed fantastical a decade ago. Spreads are tight. Distressed debt funds in Athens buy non-performing loans at five cents on the euro and exit at fifty, and the European Central Bank's balance sheet stands behind the entire arrangement like a slightly embarrassed parent at a children's party. None of this is recovery. It is the financial equivalent of vital signs on a body whose tissues are quietly necrotising, and once you understand that the patient is dying you can begin to see why the political symptoms — the censorship, the warmongering, the trade deals signed at Trump's golf courses, the institutional contempt for democratic preference — are not aberrations but functional adaptations to a structure that no longer works and whose managers have no intention of admitting it. The structural part of this story is roughly Kaldorian. The psychological part, which is the part most analysts skip past, was diagnosed with uncomfortable precision by Gustave Le Bon in 1895, and it is the missing piece that explains why the structural diagnosis cannot be acted on by the people charged with acting on it. And — this is the observation I want to develop because nobody seems to make it cleanly — the same psychological mechanism is operating on the Russian side of the war, in mirror image, with the result that the conflict in Ukraine is now being prosecuted by two ruling classes who both depend on its continuation for reasons that have very little to do with the stated objectives of either.

The story has to begin in 2008 because everything else is downstream. When Wall Street collapsed and dragged the French and German banking systems behind it, Europe faced exactly the choice that Sweden had faced in 1992 and answered the opposite way. The Scandinavian playbook from the early nineties was crude but honest: the state walked into the failed banks, nationalised them, wiped out the equity, kept the deposits whole, and re-privatised the cleansed institutions years later at a profit to the taxpayer. The bankers were not bailed out. The banks were. There is an enormous moral and economic difference between those two sentences and the entire subsequent history of the European Union turns on which one you choose. Europe chose neither. Or rather, Europe chose a third option that was effectively a coup conducted in the dark while parliaments were asleep, in which the losses of the criminal lending books in Frankfurt and Paris and Rome were transferred — without consent, without consultation, without anyone really being told what was happening — onto the shoulders of the weakest taxpayers across the union. Greek pensioners. Slovakian metalworkers. Portuguese nurses. Dutch and German workers whose real wages have been flat or falling ever since. Socialism for the bankers and a sustained programme of organised deprivation for everyone else, sold under the language of European solidarity, which is to my ear one of the more obscene linguistic inversions of the postwar period.

The mechanics of how this was administered deserve a moment because the official story — that Europe’s institutions, however imperfect, function through accountable bureaucratic process — collapses on contact with what actually happened. The European Commission, which nobody has ever accused of excessive democratic enthusiasm, was sidelined. Junker as Commission president and Pierre Moscovici as Economics Commissioner were essentially decorative. The actual decisions were taken by a much smaller body, the Eurogroup of finance ministers, and below it by the Eurogroup Working Group, an entity most European citizens have never heard of and whose chair during the critical years was an Austrian official named Thomas Wieser. Wieser ran more of Europe than the Commissioner did. He could do this because he was the only figure trusted simultaneously by Merkel and by Schäuble — those two were at war with each other for years over how brutal the medicine had to be, with Schäuble pushing for harder austerity than even Merkel could stomach — and the equidistance from both made him the actual centre of decision-making power. There was a moment when Moscovici and I had agreed on a joint proposal that would have been workable for both Greece and the eurozone, and five minutes before the Eurogroup convened I watched the Economics Commissioner of the European Union be publicly humiliated by Wieser and by Jeroen Dijsselbloem, until Moscovici was almost in tears. That is the Europe people imagine they live in. Underlings appointed through opaque procedures running the continent, the elected and quasi-elected officials reduced to props.