The Barrel That Broke the Model

Distillates, Disruption, and What the Smile Is Actually Saying

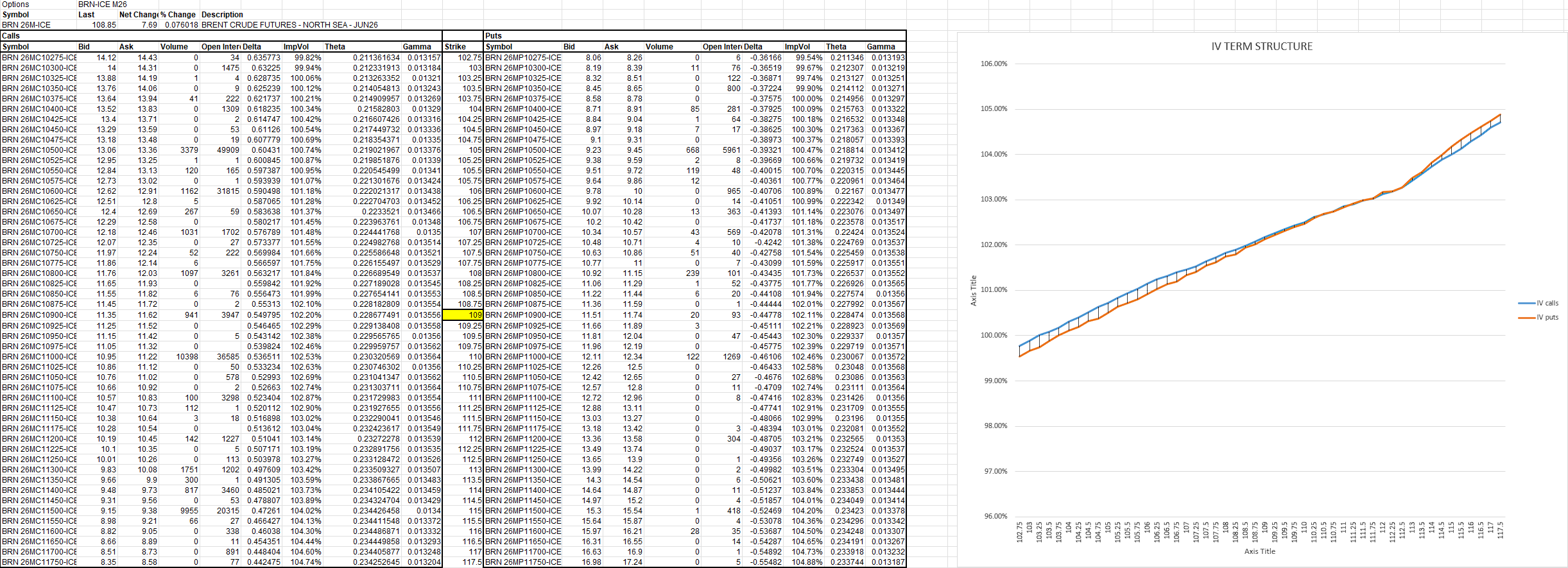

There is a particular kind of market complacency that only becomes visible in retrospect — the kind where participants price a risk premium as temporary, mean-reverting, and fundamentally tradeable, right up until the moment the physical reality underneath it makes the premium structural. We are living through exactly that transition in the distillate complex right now, and the speed at which the consensus is updating is, charitably, not impressive. But there is a second failure happening simultaneously, one layer up the analytical stack, and it is this: even the traders who have correctly identified that something unusual is happening in the physical market are misreading what the options market is telling them about it. The volatility smile on Brent is not a directional forecast. It has never been a directional forecast. Understanding what it actually encodes — and what the current shape of the ICE Brent June 2026 term structure is screaming in particular — is the difference between a hedge book that survives this cycle and one that explains itself to a risk committee.

Start with the physical architecture, because the financial market is still — inexplicably — treating this as a Brent story. It is not a Brent story. Brent is the headline, the thing that makes the evening news when it moves three percent. The real damage is happening two steps down the barrel, in jet fuel and diesel, and the mechanism is one that light-crude-processing America is structurally ill-equipped to absorb.