The Molecule Doesn't Care

Europe's energy independence is a correlated bet in a nice blue jacket — and Yamal is still writing in the volume column

Most writing about European energy is either moral or bureaucratic. This piece will try to be neither. It will treat Europe’s current position the way a portfolio manager would treat a client’s book: as a set of exposures, correlations, distributions and floors. The pictures are borrowed from a very clean thread on correlated bets. The story they tell about European gas, industry, defence financing and the 2027 Russian LNG cliff is, unfortunately, its own.

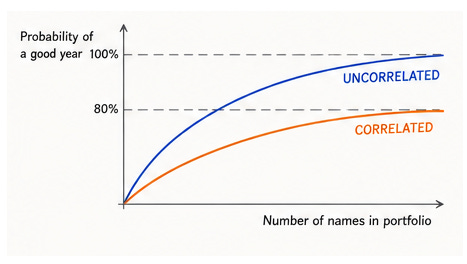

The comforting curve nobody actually lives on

Every glossy strategy document from Brussels, London and half the capitals in between reads as though Europe is walking up the blue line. Add more LNG suppliers, more terminals, more storage mandates, more sanction packages, more defence funds, more procurement schemes, more coordination mechanisms with hopeful acronyms, and the probability of a good outcome asymptotes toward one. Risk becomes a management problem. Independence becomes a project plan.

The awkward truth is that Europe is on the orange line. Its “diversified” portfolio is stuffed with names that all depend on the same underlying variable: the cost, availability and volatility of energy inputs into a mature, indebted, aging, high-cost economic bloc that is simultaneously trying to fund war, rearmament, transition and social peace. You can add as many instruments as you like. The good-year probability hits a ceiling. That ceiling is your correlation. Every additional fund only paints it in a nicer colour.

The whole rest of the essay is a description of what that ceiling looks like when you draw it properly.

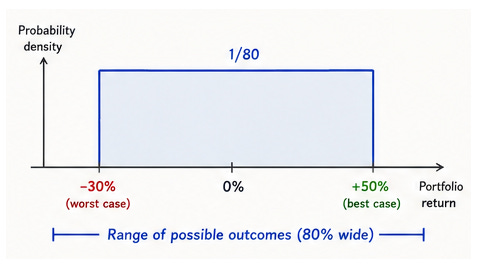

Europe’s return distribution stopped being a bell curve

Pre-2022, European industry lived under something close to a narrow bell curve. Small movements around a stable mean. Cheap, boring, reliable inputs. Cheap, boring, reliable earnings. The last political generation was built on that boredom, even though nobody labelled it that way. Cheap gas underwrote German chemicals, Italian ceramics, French metals, Dutch fertilisers, Belgian refining and Spanish electricity. Cheap gas also underwrote the welfare state, the moral vocabulary and the diplomatic self-image. Boredom, in energy terms, is a subsidy.

That distribution is gone. What replaced it is much closer to the rectangle above: a wide band of possible outcomes, roughly uniform in probability, stretching from clearly damaging on the left to comfortably profitable on the right. The mean did not disappear. It merely stopped being informative. What matters now is the width of the box.

Any serious commodity analyst would draw European power prices, TTF forward curves and industrial margins as exactly this kind of wide flat distribution. Anything narrower would be dishonest. The width itself is the story.

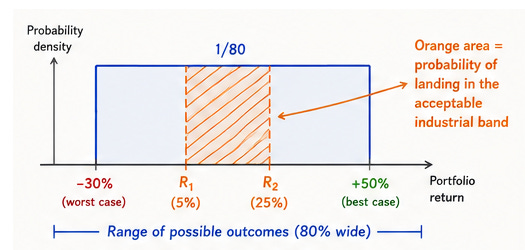

The narrow strip that keeps industry alive

Once you accept the rectangle, the useful question is no longer “what is the expected outcome?” It is: how much of the distribution is genuinely acceptable?

For European heavy industry, the acceptable band is narrower than the political conversation admits. Chemicals, fertilisers, aluminium, steel, glass, ceramics and paper do not need windfall energy. They need input costs sitting somewhere in the polite middle of the box. Call that strip R₁ to R₂. Below R₁, plants get idled, capex slips, headcount goes to Texas, and the supplier ecosystem quietly disassembles. Above R₂, upstream producers celebrate, but downstream users pass the pain to households and governments, at which point subsidy politics eats the surplus.

The orange strip in the drawing is that band. In this stylised world, the probability of landing in it is only 25%. Windfall is not rescue. Cheap gas is no longer available. The acceptable region is small, and most of the distribution is uncomfortable.

This is why record Russian LNG cargoes into the EU in H1 2026 — 136 cargoes, about 9.97 million tonnes, up 16% year-on-year, with more than 97% of Yamal deliveries going to EU ports, worth roughly €5.96bn — are not an ideological failure. They are a portfolio behaviour. When a wide box has a narrow acceptable strip, buyers rationally lift cheaper inventory while they legally can. Long-term Russian LNG contracts remain legal until 1 January 2027. In portfolio language, that is a call option with a hard expiry, and options with hard expiries always attract front-loading, no matter what the press release says.