The Road to Hell Is Paved With Oil

Why "record short crude" is a fairy tale, why the refiners are quietly loading the boat

“Well, deadbeats, shall we tumble around a bit?” — that’s how the old Soviet joke about the four-time-crashed airline captain begins, and it’s roughly the right register for what’s happening in commodities right now. Somebody in Florida wants to know whether we can compare today’s tape to the 1970s stagflation glory days, when real estate ripped, gold ripped, everything ripped, and then Volcker showed up and ruined the party. The short answer is no, and the reason is embarrassingly simple: debt. The seventies didn’t have a debt problem on the sovereign balance sheet, on the corporate balance sheet, on the household balance sheet, or really anywhere else that matters. Today, debt is the load-bearing wall of the entire structure, which means that whatever stagflationary period we’re currently enjoying will last exactly one or two quarters before it collapses into something much less romantic — a deflationary implosion where the 2008 experience will look, in retrospect, like a promotional trailer for the actual feature film. So if some clever strategist is sliding a “buy gold, buy oil, party like it’s 1974” deck across the table, thank them politely and walk out, because they’ve mistaken a rhyme for a repeat.

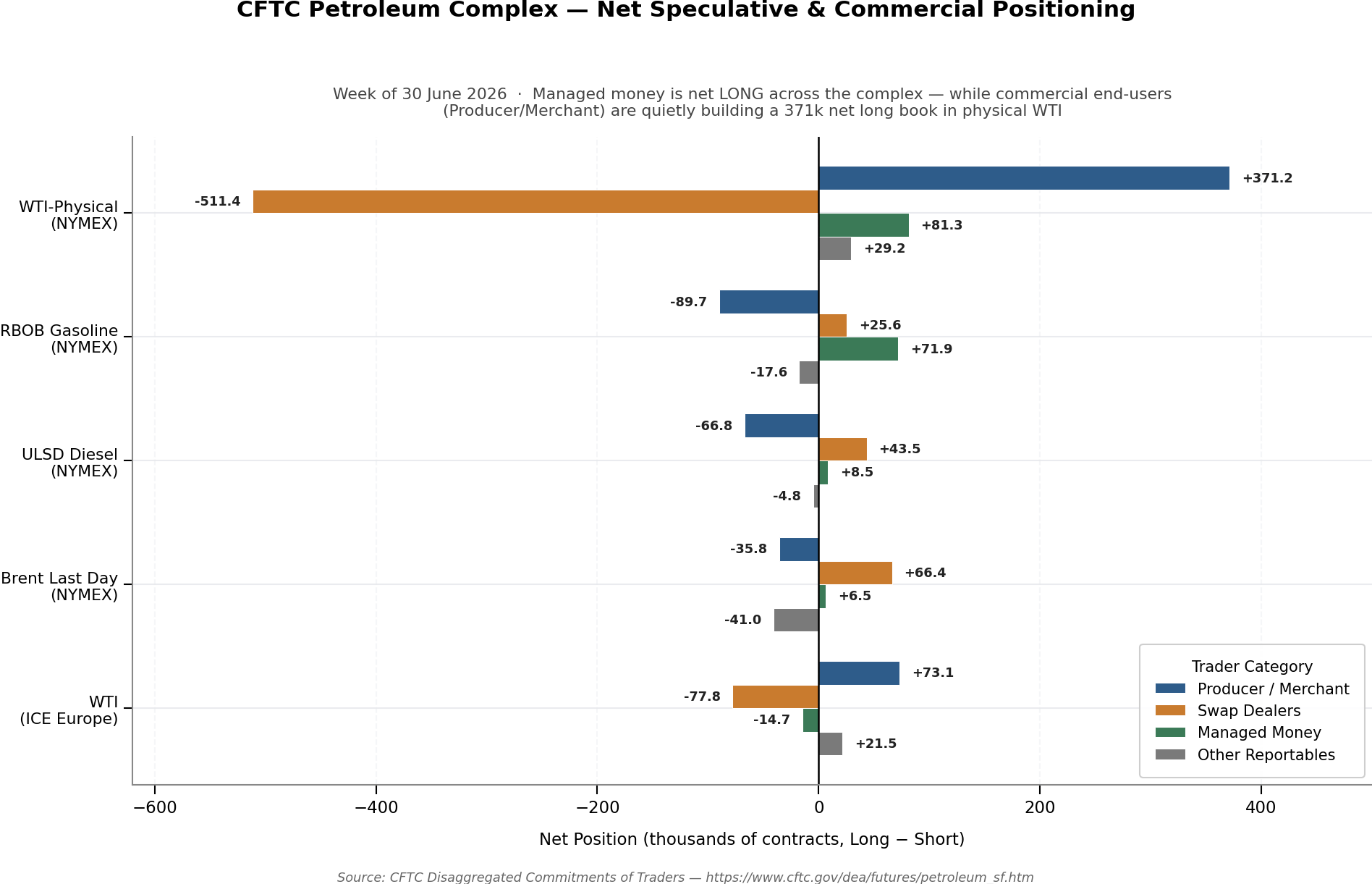

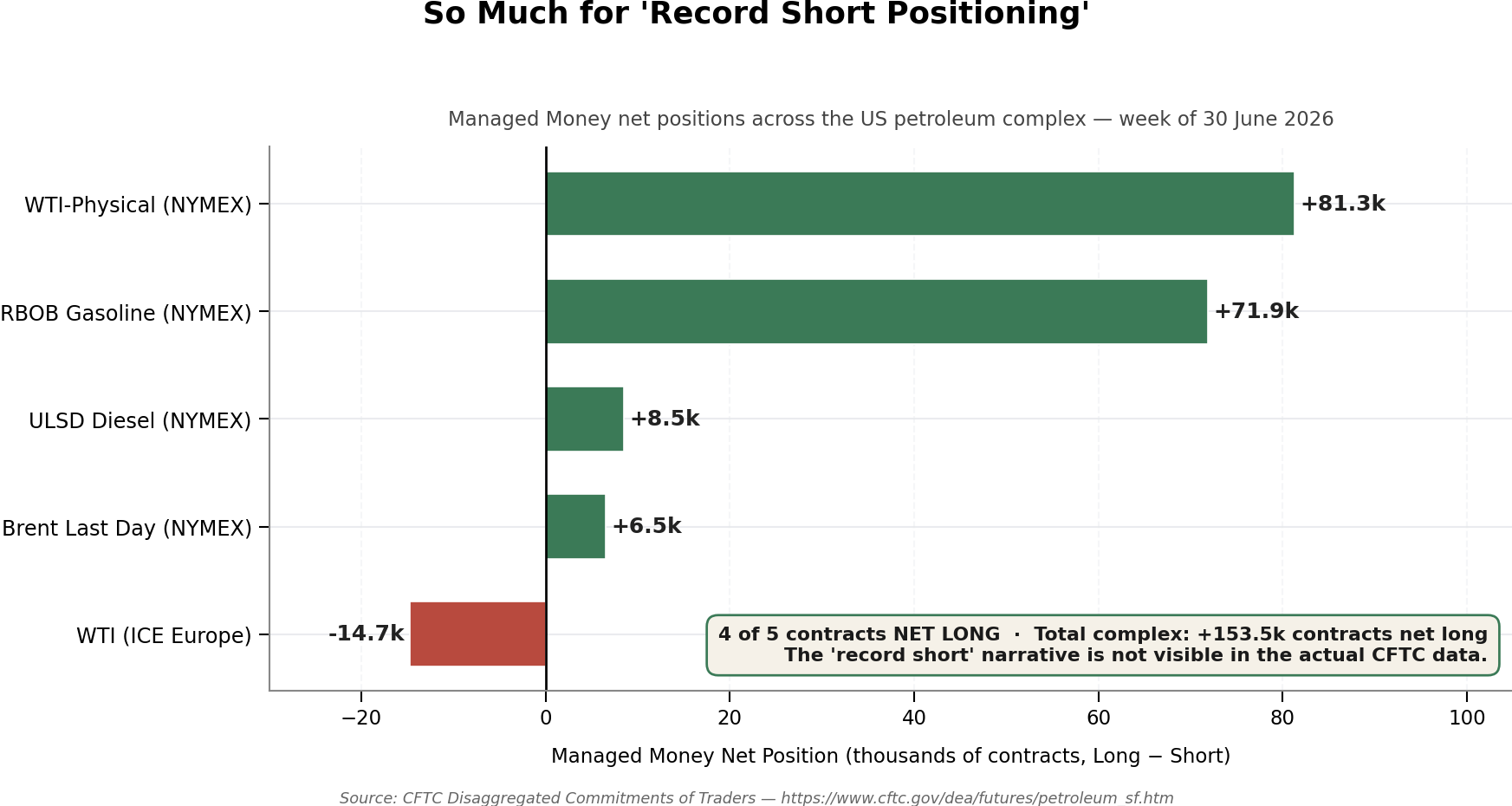

Which brings us to oil, where the consensus positioning is once again exhibiting all the elegance of a drunk on roller skates — though not in the direction the popular narrative claims. You’ll hear talking heads breathlessly quoting “record short positioning in crude,” which sounds dramatic but requires you to squint at the CFTC data through a very specific pair of goggles that quietly drop the word “gross.” Pull up the actual Disaggregated Commitments of Traders and the picture is almost the opposite. Managed money — the closest thing to a real speculator category — sits net long roughly 81,000 contracts in WTI-Physical, net long about 72,000 in RBOB gasoline, net long in diesel, net long in Brent. The paper market is comfortably positioned for calm. But dig one row down in the same report and something odd emerges: Producer/Merchant, meaning the actual refiners, blenders and physical end-users, are net long WTI-Physical by roughly 371,000 contracts. That is not what commercial hedgers do when they feel relaxed about forward barrel availability. Producers and merchants running a large net long book on physical WTI is the tell — it’s the sound of people who need actual molecules quietly reaching for the buffet tray while the paper crowd argues about macro. And in gasoline the same wrinkle appears: managed money aggressively long, commercials hedged against upside. The market is not “positioned short” — the market is positioned for a story that the commercial side is starting to doubt.

The consensus story is beautiful in the way that only a story crafted for cable television can be beautiful: peace deal with Iran, Strait of Hormuz open, Bessent riding around promising to drag Iran and Russia back into the dollar’s warm embrace because America has the deepest markets, the fairest rules, and never, ever seizes anyone’s assets. Sure, sweetheart. Meanwhile in the actual physical market, no peace has been signed — a memorandum of intentions has been signed, which is diplomat-speak for a piece of paper you can wave at cameras — and the strait, while nominally open, sees about 24-25 vessels a day, mostly Iranian tankers plus whatever floats under Iranian arrangement. Those Iranian tankers were largely feeding China, and China simply stopped buying for about a month, which is your real explanation for the recent price drop: not a supply glut, but a temporary collapse in Chinese offtake as US sanctions squeezed Iranian exports and Chinese teapot refiners got caught between government-capped fuel prices and elevated crude. Iranian production dropped twenty percent month-over-month. Nobody refines at a loss for long. So the tape got the story exactly backwards — the market interpreted a demand air pocket as a supply flood, and positioned accordingly. Congratulations to the paper longs. The refiners noticed.

The reason Trump suddenly capitulated to every Iranian condition — including terms Iran floated in April that Trump verbally accepted before promptly reneging — is that roughly two and a half weeks ago, the oil executives walked into the Oval Office and explained, with the patience one reserves for slow children, that the United States has approximately three weeks of usable crude left. Maybe enough for tonight, possibly breakfast. All that record American oil “dominance” you keep reading about? It’s been coming out of the Strategic Petroleum Reserve and commercial inventories. Cushing is empty. The SPR data is public — go look. Even accounting for the technical floor, which exists because SPR crude sits in four former salt caverns and is displaced by pumping water in from below (nice trick, since oil doesn’t dissolve salt), the geologists will tell you that once you fill more than roughly 80% of a cavern with water, you risk irreversible structural damage to the walls and you can lose the entire storage site. Do the arithmetic on the public numbers and you get, at best, about four weeks of usable inventory as of a week ago. And that’s before we get to the truly fun detail, which is that the SPR holds both light and heavy crude, and America’s much-advertised energy independence applies exclusively to the light barrels. Heavy crude — the sort you actually need if you want to produce diesel and jet fuel in industrial quantities — comes from Mexico, Canada, historically the Middle East, and a rounding error from Venezuela, where even Chevron declined to expand production because the economics don’t work and nobody knows what happens tomorrow anyway. At current consumption, the US has about eight days of heavy crude in reserve. Eight. So the American administration is now staring at a choice familiar to every declining empire in history: jet fuel or diesel? Jet fuel keeps the military and civilian aviation running; diesel keeps essentially all logistics moving. Delightful little dilemma to have right before the midterms. Trump had this politely explained to him, his modest cognitive apparatus digested the implication, and he signed whatever needed signing. Iran got everything it wanted. The son-in-law then proposed, in classic Trump-deal fashion, that the released Iranian funds be recycled into purchases of American soybeans shipped as aid to Iran, which is roughly the fiscal equivalent of paying your kidnappers in coupons redeemable at your own store.

Now to the physical reality that the futures curve is aggressively pretending doesn’t exist, but which the Producer/Merchant category apparently believes in enough to buy 371,000 contracts of. Even if we set aside the multi-month timeline required to rebuild Qatari and Kuwaiti production capacity damaged during the recent unpleasantness, the plumbing itself is broken. The Strait of Hormuz is not demined; there is a narrow passable channel and no more. Insurance underwriters will not sell coverage at anything resembling normal rates, and shipowners will not accept the risk at any rate, because insurers openly concede they have no idea what happens tomorrow — fighting could resume before your tanker clears the channel. So nobody is enthusiastically transiting Hormuz. On top of that, the tanker fleet that was parked north of the strait, unavailable to move American barrels for months, is now a technical disaster: those vessels have been sitting in warm, salty water, they’re encrusted with marine growth, and before they can load crude they need full dry-dock maintenance. Depending on age and class, that’s three to six months per hull; LNG carriers are six to nine. Meanwhile most of the tankers that used to serve the Gulf have long since been redeployed to haul American oil around the world, so they now have to reroute, wait for passage, load, and return. By any honest calculation, no meaningful new Persian Gulf supply is arriving in the physical market for at least the next two to three months. And the real problem was never crude anyway — it’s heavy crude and it’s diesel. Which is where the timing gets exquisite, because the Ukrainians, courtesy of some very helpful European deep-strike kit, have been doing remarkably efficient work on Russian refineries. Russia is now facing a genuine jet fuel problem and is openly discussing halting diesel exports. Russia handles roughly 11% of global diesel exports. That missing product has to be replaced by refineries in India, the US, Europe, and China — all of which run best on, you guessed it, heavy crude. So we are looking at physical diesel and jet fuel shortages worldwide for at least several months, developing precisely at the moment when the paper market is priced for calm and the commercial hedgers are quietly loading the boat in the opposite direction. Meanwhile potash fertilizer prices have collapsed roughly 50% — did new fertilizer supply magically materialize? No, but sure, everything is fine.

Zoom out and this is just the fourth and final step in a very well-signposted staircase into the basement. Step one was the late-nineties dot-com bubble, which popped, prompting the Fed in 2002 to launch its now-permanent “reflation initiative” — meaning just print. The real economy and labor market never fully recovered from the 2000 peak, so all that liquidity didn’t build factories, it inflated assets. Step two was the asset economy, where you bought a house with 20% down, watched it appreciate 50%, refinanced at the higher valuation, extracted cash, and bought a Ferrari — red, not yellow, because midlife crisis has standards — and then did it again, and again, until mortgages had been issued to anyone with a pulse and the whole edifice detonated in 2008. Step three was the transfer of private losses to sovereign balance sheets — privatize the gains, socialize the losses, and stand back while sovereign debt crises rolled through the weakest links: Greece, Cyprus, the usual suspects. Central bank response: more liquidity, because that’s the only tool in the box. And now we’re on step four, which is a bubble in sovereign debt itself, layered with a bubble in “AI-driven growth” in the United States where hyperscalers are pouring hundreds of billions of borrowed capital into data centers and adjacent energy infrastructure to the point where, for the first time, the GDP contribution from this activity has exceeded the contribution from consumer spending — which is, incidentally, shrinking. The AI thing is a genuinely useful technology in narrow applications, but roughly 56% of US banks are now quietly rehiring the people they fired trying to replace them with models, because it turns out the marketing was somewhat ahead of the product. We’ve done this before — Big Data was going to change everything, blockchain was going to change everything, both found niches spectacularly smaller than the invested capital would justify, and private equity, which was funding much of this cycle, is now watching redemption requests exceed inflows for the first time. Same picture, different framing.

The endgame is unpleasant in a very specific way. Every prior crisis was solved by shifting the risk onto a more reliable counterparty, and the government was always the last reliable counterparty. But governments themselves no longer look reliable — not American, not European, not really anyone — because the numbers stopped working. The headline US federal debt is roughly $40 trillion, but the unfunded liabilities for Social Security, Medicare, and the rest add another $70 trillion in present-value terms. Call it $110 trillion, minimum. There is exactly one exit from that: monetize everything, which is the polite Austrian term for a race to the bottom in fiat currencies. Some genius came up with the “Mar-a-Lago Accords” theory — the notion that we can replicate the post-WWII trick where nominal GDP grew 3-4% faster than debt and quietly deflated the ratio — but that plan requires a capex boom, a weaker dollar, and effective tariffs, and so far the tariffs are being paid by American consumers (with $150-160 billion now potentially owed back to importers as refunds), the dollar refuses to weaken, and the long end of the curve keeps climbing. Meanwhile the collateral damage from elevated oil, diesel, and gasoline prices is stripping FX reserves out of every country that isn’t a net energy exporter — Turkey already burned through its bonds and is now dumping gold, Japan is dumping US paper because it holds so much it may never need to touch bullion — creating the perverse dynamic where the dollar actually rallies into the deflationary phase as everyone scrambles for greenbacks to service dollar debts and buy energy at elevated prices. Only after that does the currency itself get slaughtered. Britain and France are already textbook cases with visible cash-flow gaps in the budget that can only be closed by destroying social spending or defaulting; the IMF can’t save them because the IMF will show up and demand exactly that. America is next in that queue, whether it realizes it or not. So the setup, if you’re a commodities person, is roughly this: managed money comfortably long across the petroleum complex while physical end-users are quietly building a 371,000-contract net long book in WTI that they wouldn’t be building if they believed the calm-supply story, heavy crude going structurally scarce right as Russian refinery outages force diesel replacement demand into the same barrel pool, potash mispriced on the downside for no good reason, precious metals being accumulated by central banks and by Turkey-style scramblers, sovereign curves creaking under weight they can’t carry, and an equity market where the growth story is a mirage funded by borrowed money that’s beginning to demand its return. As Vasily Ivanovich once told Petka while explaining optics: there is a nuance. And the nuance this time is that the deadbeats have already boarded, the captain is bandaged and cheerful, the commercial hedgers are quietly checking their parachutes, and we are cleared for takeoff. Buckle up.