UAE Has Left the Group Chat

Dollar Swaps, Fujairah Loadings, and the End of OPEC as We Knew It

Last week was that moment, a particular kind of moment when several stories run in parallel creating the right amount of white noise.

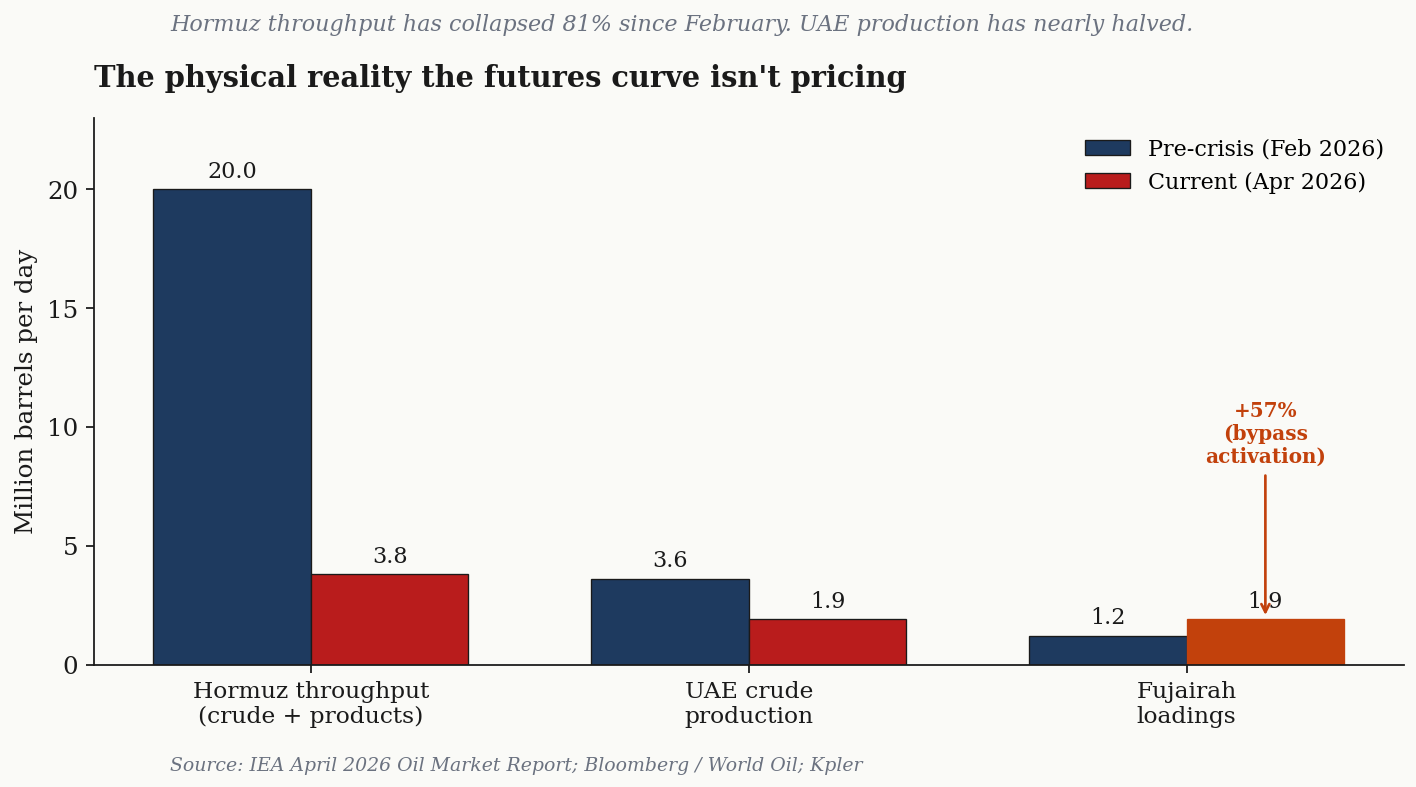

Treasury Secretary Bessent stood in front of Congress and admitted, with the kind of carefully bureaucratic language that always means the opposite of what it says, that the Federal Reserve was negotiating dollar swap lines not just with the United Arab Emirates but with “many of our Gulf allies” and “numerous other countries, including some of our Asian allies.” Three days later, on April 28, the UAE state news agency WAM confirmed what had been rumoured all spring: Abu Dhabi is leaving OPEC and OPEC+ effective May 1, ending a membership that began in 1967, four years before the federation itself was formally established. And underneath both announcements, the physical oil market was doing something that the front of the Brent curve has only haltingly acknowledged: dated North Sea Brent has been trading around $130 a barrel, roughly $60 above pre-conflict levels, while the Strait of Hormuz, which used to move twenty million barrels a day of crude and products, has collapsed to under four million. The IEA’s April 2026 Oil Market Report, in language that is unusual for that institution, calls it the largest disruption in history. Tanker traffic through the strait is effectively zero. Nearly two thousand vessels are stranded in the Persian Gulf. VLCC charter rates have run up six times their pre-crisis level. P&I clubs have suspended war risk cover for vessels entering the strait, which is the insurance industry’s polite way of saying that no rational owner sends a ship in there anymore. War risk premiums, when they can be obtained at all, have moved from a quarter-point of vessel value per transit to commercially prohibitive territory. This is not a slowdown. This is a chokehold.