Volga

Volga’s universal relevance—from Wall Street to international shipping lanes.

In financial derivatives, traders traditionally rely on first-order Greeks like Delta and Vega to assess risk. However, second-order Greeks such as Volga (volatility gamma) reveal why nonlinear responses to volatility shifts create unique opportunities and risks.

This article explores Volga’s role in pricing Asian options—exotic derivatives tied to average asset prices—and its implications for freight markets, where volatility in shipping rates impacts global trade. By bridging quantitative finance and logistics, we uncover how Volga shapes risk management strategies across industries.

The Foundation: Vega and Volga in Option Pricing

Vega’s Limitations in Nonlinear Environments

Vega measures an option’s price sensitivity to changes in implied volatility (IV). For example, an Asian call option with a Vega of $0.10 gains $0.10 if IV rises by 1%10. However, Vega assumes linearity, ignoring how volatility shifts alter the sensitivity itself. This is where Volga becomes critical:

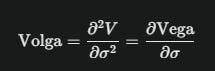

Volga quantifies the convexity of Vega—i.e., how Vega accelerates or decelerates as volatility changes.